You’ve done your research, and you’re ready to purchase a home. Your credit report hits the mark, so now you’re ready to start checking out mortgage loan options. This loan can take years to pay off, so it’s a good idea to shop around to pick the best option for you.

Credit scores play a large role in the cost of a mortgage. If the score is lower, it may contribute to higher interest rates and a higher monthly mortgage payment.

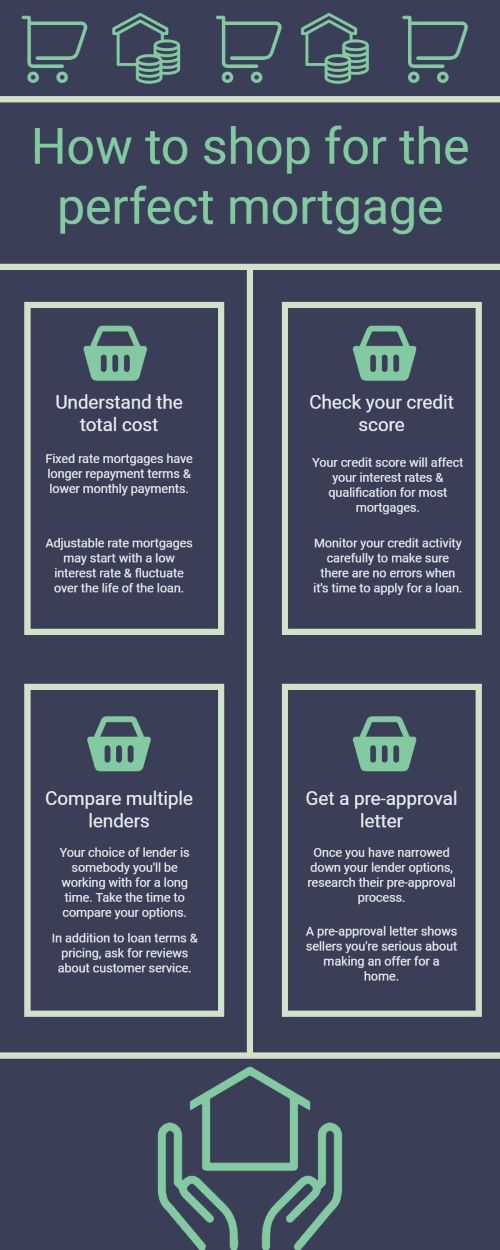

A fixed rate mortgage is a great option if you don’t want the interest rate to alter with time. This type of loan has a preset rate, which is typically paid over the span of 15 or 30 years. Longer loan terms will decrease your monthly payment. Over the lifespan of this loan, the interest rate will remain constant.

Adjustable rate mortgages may start with a fixed interest rate, but are subject to change. This means if the insurance and property tax increase over time, you may see this included in the mortgage payment. Mortgages are made up of your property tax, principal, insurance and interest rates. Changes to any of these factors can affect your monthly payment.

Your credit score will help a mortgage lender determine if you’re qualified to take on the loan and can handle the interest rates involved. You want to stay on top of checking your credit history to make sure the score is where it should be. A history of paying your bills on time will work in your favor.

There are so many options available - it isn’t enough to just know the monthly payment. Finding the right fit for a mortgage lender can be a tricky process.

Consult your real estate agent for suggestions. They often have experience with multiple lenders, so they can help you create a list of firms fitting your criteria. This will provide the opportunity to compare interest rates, monthly payments and figure out which option is best for you.

Once you have narrowed down your lender prospects, research their pre-approval letter process. Make sure your credit score is acceptable and then request an approval letter. A pre-approval letter is not an official offer for a loan, but signifies a lender has inquired about your financial state and affirmed you meet requirements to be offered funding. Having a pre-approval letter also shows sellers you’re serious about putting in a valid offer for their property.

When you’re ready to buy a house, check and compare quotes and negotiate loan rates. Make sure your credit score is at a place accepted by most lenders. Once you have found a potential lender, you’ll be well on your way to homeownership.

As a lifelong resident of Litchfield County, Heather is quite familiar with the beautiful Northwest Corner of Connecticut. In partnership with her husband at Turri, Inc., in Torrington, she managed and grew a 30+ employee electrical contracting firm that served both the residential, commercial and industrial industries. Currently residing in Goshen she hopes to transfer and utilize many of the skills she learned in contracting to the real estate industry.

Knowing how a vital community relies on its volunteers, Heather spent many hours in several capacities at local organizations that she admires. She serves on the Woodridge Lake Finance Committee and House Committee, Victoria Court Condominium Association (secretary) and Educating Canines Assisting with Disabilities (volunteer and nursery mom). Heather has also been involved with Goshen Community Care & Hospice (president of board of directors), Warner Theatre (board of directors), LARC (volunteer), Festival of Trees (founder), the Northwest Chamber of Commerce, and Goshen Business Circle. Heather also served as Vice President of Woodridge Lake’s Board of Directors.

In Heather’s spare time, she enjoys spending time with family usually in an active way by playing tennis, golf, boating, hiking and skiing.

Heather is honored to be a part of the E.J. Murphy team and hopes you will contact her with any of your real estate needs.